Five decades of strategic property investment across Asia-Pacific and North America — defined by contrarian conviction, impeccable timing, and an unwavering belief in the enduring value of prime land.

Oei Hong Leong approaches real estate with the same intellectual rigour and contrarian instinct that has defined his career across bond markets, equities, and corporate acquisitions. Where most investors follow consensus, Oei studies cycles. Where others see risk, he identifies asymmetry. His property portfolio — spanning the most coveted addresses in Singapore, landmark developments in Vancouver, and strategic holdings across the Asia-Pacific — is the physical manifestation of a philosophy forged over five decades of navigating the world's most volatile markets.

At the heart of his approach lies a deceptively simple conviction: land in prime locations is the ultimate store of value. Unlike currencies that can be debased, equities that can collapse, or bonds that can default, well-located real estate in global cities possesses an intrinsic scarcity that only deepens with time. Singapore's limited land mass, Vancouver's geographic constraints between ocean and mountains, Hong Kong's density — these are not market inefficiencies to be exploited. They are permanent structural advantages to be owned.

Oei's investment philosophy rejects the frenetic pace of modern real estate speculation. He does not flip properties. He does not chase yield. He acquires assets with generational time horizons, holds them through downturns that would shake lesser investors, and develops them only when the convergence of market conditions, regulatory frameworks, and strategic vision creates the conditions for transformative value creation. This patience — this willingness to endure years, even decades, of carrying costs and political headwinds — is perhaps his greatest competitive advantage.

Singapore is the bedrock of Oei Hong Leong's real estate portfolio and the city-state where his property instincts were first honed. Through his flagship holding company, Chip Lian Investments, and a network of related entities, Oei has assembled one of the most formidable private property portfolios in Southeast Asia — concentrated in the prime districts that define Singapore's skyline and commercial identity.

Oei's residential holdings are concentrated in what Singaporeans call the Golden Triangle — the prime districts of Orchard Road (District 9), Bukit Timah and Holland (District 10), and Newton and Novena (District 11). These are not merely prestigious addresses; they are the districts where land supply is at its most constrained, foreign buyer demand is at its most resilient, and the gap between replacement cost and market value offers the most compelling risk-adjusted returns.

His acquisitions in these districts have followed a consistent pattern: identify undervalued parcels during market downturns, acquire at prices that discount future development potential, and hold with conviction through subsequent cycles. Several of his most significant Singapore residential assets were acquired during the Asian Financial Crisis of 1997–98 and the Global Financial Crisis of 2008–09, periods when distressed sellers and fearful capital markets created opportunities invisible to all but the most disciplined investors.

The portfolio includes freehold and 999-year leasehold properties — tenure structures that Oei particularly favours for their perpetual optionality. Unlike 99-year leaseholds, which depreciate as they age, freehold properties in Singapore's prime districts have demonstrated a consistent ability to appreciate through multiple property cycles, serving as both inflation hedges and intergenerational wealth vehicles.

Beyond residential holdings, Oei maintains significant positions in Singapore's commercial property market. His commercial portfolio includes office buildings in the Central Business District, retail frontage along Orchard Road, and mixed-use developments that straddle the line between commercial yield and residential capital appreciation. These assets generate the steady rental income that underpins his broader investment activities while benefiting from Singapore's status as Asia's premier financial hub.

The commercial holdings reflect a nuanced understanding of Singapore's evolving urban fabric. As the city-state has transformed from a regional trading post into a global wealth management centre and technology hub, Oei's commercial properties have benefited from rising Grade A office rents, increasing demand for premium retail space, and a regulatory environment that consistently favours property owners through measured supply management.

Notably, Oei has been a long-standing advocate of Singapore's Urban Redevelopment Authority masterplanning process, which he views as one of the critical factors differentiating Singapore real estate from other Asian markets. The government's systematic approach to land use planning, infrastructure investment, and supply calibration creates a predictability rare in emerging Asian property markets — a predictability that sophisticated investors can underwrite with confidence.

One of the less visible but equally significant components of Oei's Singapore strategy is his approach to land banking and en bloc acquisitions. Singapore's en bloc (collective sale) market — where ageing condominiums are sold collectively to developers for redevelopment — has been a recurring source of opportunity for astute investors with the patience and capital to participate.

Through carefully structured acquisitions of units within older developments, Oei and his entities have positioned themselves to benefit from the cyclical waves of en bloc activity that periodically sweep through Singapore's property market. This strategy demands a unique combination of legal sophistication, neighbourhood-level market intelligence, and the financial capacity to hold positions for extended periods while collective sale processes unfold — often a matter of years rather than months.

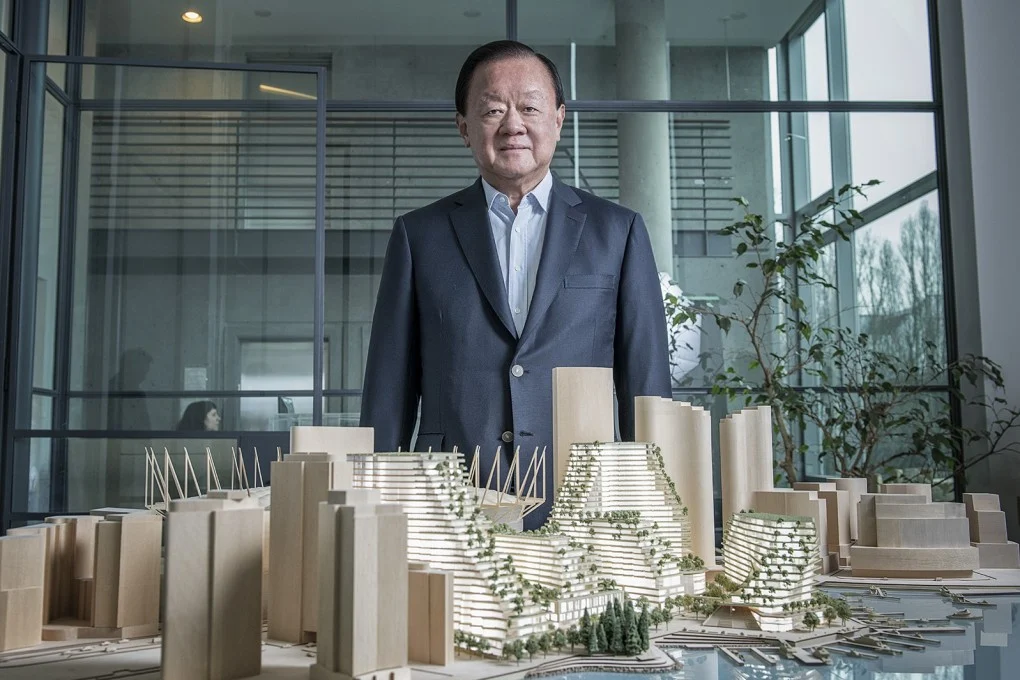

No single asset in Oei Hong Leong's portfolio better encapsulates his investment philosophy — the boldness, the patience, the willingness to endure controversy, and the ultimate conviction in location value — than the Plaza of Nations in Vancouver, British Columbia. It is a story of vision colliding with politics, of international capital meeting local resistance, and of one man's refusal to abandon a thesis he believed in absolutely.

The Plaza of Nations sits on approximately 6.2 acres of prime waterfront real estate along the north shore of False Creek in downtown Vancouver, one of the most desirable parcels of undeveloped land in any major North American city. Originally built as the Expo 86 pavilion — the centrepiece of Vancouver's 1986 World Exposition — the site had fallen into a state of disuse and underinvestment by the time Oei Hong Leong entered the picture.

Oei acquired the site through a series of transactions in the mid-2000s, reportedly paying in excess of CAD 80 million for the combined parcels. At the time, the acquisition raised eyebrows. The site was encumbered by complex zoning restrictions, its entertainment and event-space tenants generated modest income relative to the land value, and the political environment surrounding waterfront development in Vancouver was fraught with uncertainty. To most observers, it was a property with immense theoretical potential but daunting practical challenges.

To Oei, however, the calculus was straightforward. The site enjoyed approximately 800 feet of unobstructed waterfront along False Creek, sat immediately adjacent to downtown Vancouver's soaring residential towers, and occupied what would inevitably become the final major redevelopment parcel on one of the world's most spectacular urban waterfronts. The question was never whether the land would become extraordinarily valuable. The question was when — and under what conditions.

Oei's investment thesis for the Plaza of Nations rested on three pillars that reflect his broader approach to property investment. The first was absolute scarcity. Vancouver is geographically constrained by mountains to the north, ocean to the west, the U.S. border to the south, and the Agricultural Land Reserve to the east. Within this already limited geography, waterfront parcels of the scale and centrality of the Plaza of Nations simply do not exist. Once developed, the site would possess a permanent monopoly on its particular combination of water views, downtown proximity, and development scale.

The second pillar was demographic inevitability. Vancouver's population growth, driven by both domestic migration and international immigration — particularly from Asia-Pacific markets familiar to Oei — was creating sustained demand for premium residential and mixed-use space in the downtown core. The third pillar was the maturation of Vancouver as a global city. The 2010 Winter Olympics, growing technology sector investment, and the city's emergence as a destination for global capital all pointed toward long-term appreciation in prime real estate values.

Oei envisioned transforming the site into a mixed-use development of extraordinary ambition — a waterfront precinct combining luxury residential towers, premium retail and dining, public open space, and cultural amenities that would rival the finest waterfront developments anywhere in the world. The development, in his vision, would not merely occupy the site but would define a new chapter in Vancouver's evolution as a global city.

The development journey for the Plaza of Nations has been one of the most protracted and politically complex in Vancouver's modern history. Over the course of nearly two decades, multiple development proposals have been submitted, debated, revised, and resubmitted in a process that has tested the patience and resolve of even an investor of Oei's temperament.

Early proposals called for a series of residential towers ranging from 30 to 60 stories, designed by internationally renowned architects, with significant ground-level retail and public amenities. These plans were met with opposition from neighbourhood groups concerned about density, shadow impacts, and the perceived loss of public waterfront access. Successive iterations of the development proposal sought to address these concerns through increased public open space, reduced tower heights, and enhanced community benefit commitments.

The site's unique position within Vancouver's urban fabric has made it a lightning rod for the broader tensions that define waterfront development in major global cities: the competing interests of private landowners, public access advocates, heritage preservation groups, housing affordability campaigners, and the municipal governments that must mediate between them. Each of these constituencies has had views on what the Plaza of Nations should become, and the planning process has been shaped by the friction between these visions.

The property's existing entertainment venues, including a performance space and event facilities, have added a further layer of complexity. These tenants, while generating relatively modest income relative to the site's potential highest and best use, have created cultural attachments and community expectations that any development proposal must navigate carefully. Managing the transition from an underutilised entertainment precinct to a world-class mixed-use development has required diplomatic skills as much as financial ones.

Perhaps the most significant factor shaping the Plaza of Nations saga has been the political environment in Vancouver and, more broadly, in British Columbia. The past two decades have witnessed a dramatic shift in public attitudes toward real estate development, foreign investment in property, and the role of international capital in shaping Canadian cities. These shifts have had direct and material implications for Oei's development plans.

The introduction of British Columbia's foreign buyer tax in 2016, the speculation and vacancy tax in 2018, and a series of increasingly restrictive development approval processes have altered the economic calculus for international property investors. While these measures were primarily targeted at speculative residential buyers rather than long-term development investors like Oei, they contributed to a political climate in which foreign ownership of prime urban land became a subject of intense public scrutiny.

Vancouver's municipal politics have further complicated the picture. Successive city councils have oscillated between pro-development and slow-growth orientations, creating an unpredictable approval environment for major projects. The Plaza of Nations, given its waterfront prominence and the scale of proposed development, has been particularly susceptible to these political currents. Development applications have had to navigate not only technical planning requirements but also the shifting ideological priorities of elected officials.

Through all of this, Oei has maintained his position with characteristic resolve. Where other international investors might have abandoned the project in frustration, he has continued to engage with the planning process, refine development proposals, and absorb the carrying costs of holding one of North America's most valuable undeveloped parcels. His willingness to endure this extended timeline speaks to a fundamental conviction that the ultimate value of the site will justify the years of patience.

As of the mid-2020s, the Plaza of Nations remains one of the most consequential undeveloped sites in Vancouver — a status that, paradoxically, has only enhanced its long-term value proposition. In the years since Oei's acquisition, the surrounding neighbourhood has been transformed. The adjacent concord Pacific Place and Southeast False Creek developments have created a dense residential community immediately next to the site. The construction of the Canada Line rapid transit, Olympic Village infrastructure, and the broader revitalisation of False Creek have all contributed to a sustained increase in land values in the immediate vicinity.

The site's development potential, when eventually realised, is likely to be one of the most significant value-creation events in Canadian real estate history. Conservative estimates suggest the fully developed property could yield residential and commercial space valued in excess of CAD 3–4 billion at current market prices — a multiple of several times the original acquisition cost and accumulated carrying charges. This outcome, while still contingent on development approvals and market conditions, illustrates the extraordinary leverage that patience confers upon the holder of irreplaceable urban land.

Looking ahead, several factors favour the eventual realisation of the site's potential. Vancouver's chronic housing undersupply, the growing political consensus that major development sites must be activated to address the housing crisis, and the continued appreciation of waterfront property values all point toward a more favourable environment for the Plaza of Nations' development. The question confronting Oei and his team is no longer whether the site will be developed but rather what form the development will take and how it will integrate with the evolved expectations of Vancouver's community and government.

The Plaza of Nations saga offers profound lessons for students of real estate investment, urban planning, and the intersection of international capital with local politics. For Oei, the experience has reinforced several core tenets of his investment philosophy while also revealing the limits of financial conviction in the face of political and regulatory complexity.

Lesson one: The irreplaceable nature of prime location endures through all political and economic cycles. Despite nearly two decades of regulatory uncertainty, the fundamental value proposition of the Plaza of Nations site has only strengthened. No amount of political opposition can diminish the physical reality of 6.2 acres of waterfront land in the heart of a growing global city.

Lesson two: International real estate investment demands cultural and political intelligence that extends far beyond financial analysis. The carrying costs of the Plaza of Nations have been not merely financial but reputational, requiring sustained engagement with local communities, media, and government at a level of intensity that many foreign investors underestimate.

Lesson three: Patience is not merely a virtue in real estate — it is a competitive advantage. The capacity to absorb years of uncertainty, carrying costs, and political friction while maintaining conviction in a long-term thesis is a form of capital in itself — and one that is exceedingly rare among institutional and private investors alike. Oei's ability to hold the Plaza of Nations through multiple property cycles, political administrations, and regulatory changes has created a moat around the asset that no competitor can replicate.

Lesson four: The convergence of development timing and political will is ultimately what determines the realisation of value in complex urban sites. The most visionary development plan is worthless without the regulatory approvals to execute it, and those approvals are granted not on the basis of financial analysis but on the basis of political judgment. Managing this reality — with patience, diplomacy, and strategic flexibility — is the essential skill of large-scale urban development.

Beyond Singapore and Vancouver, Oei Hong Leong has maintained a selective but significant presence in international property markets, applying the same principles of location scarcity, cycle timing, and patient capital that define his core portfolio.

Hong Kong, with its extreme land scarcity and unique position as the interface between global capital markets and the Chinese economy, has been a natural extension of Oei's property investment thesis. His Hong Kong interests have historically focused on prime commercial properties in the Central and Admiralty districts, as well as selective residential positions in the Mid-Levels and Peak areas. These holdings have benefited from Hong Kong's sustained role as Asia's premier international financial centre, even as political developments have reshaped the territory's relationship with mainland China.

Oei's approach to Hong Kong property has mirrored his Singapore strategy — focusing on freehold or long-term leasehold assets in locations where supply constraints create natural price floors. His willingness to invest in Hong Kong during periods of political uncertainty, when other international investors retreated, reflects the same contrarian instinct that has defined his most successful acquisitions globally.

Australia's major cities, particularly Sydney and Melbourne, have featured in Oei's international property calculus. The Australian market offers a combination of attributes that align with his investment criteria: transparent legal systems, strong population growth driven by immigration, limited prime urban land supply, and a currency that has historically provided diversification benefits for Singapore-dollar-denominated investors. His Australian interests have focused on commercial properties in Sydney's CBD and selective residential development sites in premium suburban locations.

As one of Singapore's most experienced property investors, Oei has naturally maintained an awareness of opportunities across the broader ASEAN region. While his core holdings remain concentrated in Singapore and developed markets, selective investments in Malaysia, Thailand, and Indonesia have provided exposure to the rapid urbanisation and rising affluence of Southeast Asia's emerging middle class. These positions have typically been structured through local partnerships and joint ventures, reflecting an understanding that regional property markets demand local expertise and relationships that complement international capital.

If there is a single skill that distinguishes Oei Hong Leong from the vast majority of property investors, it is his relationship with time. Most real estate investors operate on cycles of five to seven years — buying at what they perceive as the bottom, developing or repositioning, and selling at what they hope is the top. Oei operates on cycles of decades.

His track record reveals a consistent pattern of acquiring assets during periods of maximum pessimism. The Asian Financial Crisis of 1997–98, the SARS-driven market collapse of 2003, the Global Financial Crisis of 2008–09, and the COVID-19 disruption of 2020–21 were all periods during which Oei was deploying capital rather than retreating. This counter-cyclical discipline is not merely temperamental — it is analytical. Oei studies property cycles with the same intensity that he brings to bond markets and currency movements, identifying the inflection points where sentiment has diverged most dramatically from fundamental value.

His approach to selling is equally disciplined. Unlike speculative investors who attempt to time the peak of each cycle, Oei rarely sells core holdings. His philosophy holds that the transaction costs of selling — including capital gains taxes, reinvestment risk, and the loss of a proven asset — almost always exceed the marginal benefit of capturing a cyclical peak. Instead, he manages portfolio risk through leverage adjustment, using low-interest-rate environments to lock in long-term financing and high-rate environments to reduce borrowing.

Many of the most valuable properties in the Oei portfolio today were acquired during periods when headlines screamed of collapse and peers were liquidating positions. These crisis-vintage acquisitions have generated the highest returns in the portfolio precisely because they were purchased at moments of maximum fear and minimum competition. It is a strategy that requires not just analytical conviction but emotional fortitude — the willingness to sign contracts and deploy capital when every instinct suggests retreat.

Oei's commercial property strategy is predicated on income generation and inflation protection. Grade A office buildings in Singapore's CBD, retail properties along established shopping corridors, and mixed-use developments with strong tenancy profiles provide the steady cash flows that underpin his broader investment activities. Commercial properties, in his framework, are the portfolio's engine — generating the income that funds new acquisitions, services debt, and provides liquidity during market downturns.

His commercial acquisitions favour properties with long-term leases to creditworthy tenants, structures that provide built-in rental escalation mechanisms, and locations where supply constraints ensure sustained tenant demand. He has been particularly astute in identifying commercial properties where the land value significantly exceeds the value of the existing improvements — creating embedded optionality for future redevelopment.

Residential property, in Oei's portfolio, serves a fundamentally different purpose. Residential assets are capital appreciation vehicles — purchased not for their income yields, which are typically modest in prime Asian markets, but for their long-term price appreciation potential. In Singapore, where residential property prices in prime districts have compounded at rates that significantly exceed inflation and rival equity market returns over multi-decade periods, residential real estate functions as a cornerstone of wealth preservation.

The residential strategy also reflects a deep understanding of the social and cultural dynamics of Asian property markets. In Singapore, Hong Kong, and much of the Asia-Pacific, residential property ownership carries cultural significance that transcends pure financial calculation. Prime residential addresses confer social status, intergenerational security, and a tangible connection to place that no financial instrument can replicate. Oei's residential holdings leverage these cultural dynamics alongside traditional financial metrics.

Oei Hong Leong's commitment to real estate as a wealth preservation vehicle is informed by a lifetime of observing the impermanence of other asset classes. Having witnessed the destruction of wealth through currency crises, sovereign debt defaults, equity market collapses, and the erosion of purchasing power through inflation, he has concluded that well-located property offers a form of security that no paper asset can match.

This conviction is not merely theoretical. The Oei family's history — spanning the upheavals of mid-twentieth-century Southeast Asian politics, the volatility of post-colonial economic development, and the recurring financial crises that have punctuated Asia's growth story — has instilled a profound appreciation for the durability of physical assets. When currencies collapse, real estate remains. When governments change, the land endures. When markets crash, the addresses retain their prestige and their scarcity.

In practical terms, Oei's wealth preservation strategy through real estate manifests in several ways. He favours assets with minimal ongoing capital expenditure requirements — well-built properties in established locations that do not demand constant reinvestment. He maintains conservative leverage ratios, ensuring that his properties can withstand extended periods of rental income decline without triggering covenant breaches or forced sales. And he structures ownership through entities that provide tax efficiency, succession planning flexibility, and protection against jurisdictional risks.

The portfolio's geographic diversification across Singapore, Canada, Hong Kong, and Australia provides a further layer of preservation. By holding prime assets across multiple jurisdictions with independent legal systems, currencies, and economic cycles, Oei has constructed a real estate portfolio that is resilient to any single country's political or economic disruption — a form of sovereign risk management executed through brick and mortar rather than financial derivatives.

Oei's current assessment of the Singapore property market reflects cautious optimism grounded in structural analysis. The city-state's growing role as Asia's premier wealth management centre, the influx of family offices and high-net-worth individuals relocating from Hong Kong and mainland China, and the government's measured approach to new land releases all support a constructive long-term outlook for prime property values. The cooling measures periodically imposed by the Singapore government — including Additional Buyer's Stamp Duty increases, Total Debt Servicing Ratio limits, and foreign buyer restrictions — are viewed not as threats but as stabilising mechanisms that prevent the speculative excesses that destroy value in other Asian markets.

The key risk Oei monitors in Singapore is the potential for interest rate normalisation to compress property valuations, particularly in segments where yields are already thin. However, his long-term holding approach and conservative leverage provide substantial insulation against this risk, and his crisis-vintage acquisition prices provide a margin of safety that more recent market entrants do not enjoy.

Looking across the global property landscape, Oei identifies a market environment characterised by significant divergence. The post-pandemic period has created distinct dynamics across different property sectors and geographies. Prime residential property in global gateway cities has demonstrated remarkable resilience, driven by wealth concentration, limited supply, and the enduring desire of the world's affluent to anchor themselves in the most desirable urban locations.

Commercial property, by contrast, faces more complex headwinds. The structural shift toward remote and hybrid work has created uncertainty around office demand in many markets, while the evolution of retail toward experiential and omnichannel formats has challenged traditional retail property valuations. Oei's commercial holdings have been relatively insulated from these trends given their concentration in Singapore, where office attendance rates have recovered more fully than in Western markets and where the government's pro-business orientation supports continued demand for premium office space.

Looking ahead, Oei's market perspective suggests that the most compelling opportunities in global real estate will emerge at the intersection of urbanisation, infrastructure investment, and the energy transition. Cities that are investing in transit connectivity, sustainable building standards, and quality of life amenities will attract the talent and capital that drive property values. His own portfolio, concentrated in Singapore and Vancouver — two cities that rank among the world's most liveable and infrastructure-rich — is well positioned to benefit from these long-term secular trends.

After five decades of navigating property cycles across multiple continents, Oei Hong Leong's investment principles have been distilled to their essence. Buy scarcity. Prime locations do not lose their primacy. Hold with conviction. The greatest returns in real estate accrue to those who resist the temptation to trade. Be greedy when others are fearful. The best acquisitions are made when headlines are darkest and competition is thinnest. Respect the cycle, but do not try to time it. Property markets are mean-reverting; the investor's task is to survive the troughs and participate in the peaks.

These principles, forged in the crucible of Asian financial crises, tested across four countries and multiple property sectors, and validated by a portfolio whose value has compounded across decades, represent the distilled wisdom of one of Asia's most experienced property investors. They are simple in articulation but extraordinarily difficult in execution — demanding a combination of analytical rigour, emotional discipline, financial capacity, and temporal patience that few investors possess.

For Oei, real estate has never been merely an investment class. It is a philosophy — a belief that the most enduring form of wealth is that which is anchored in the earth itself, in the irreplaceable locations where human activity concentrates and prosperity compounds. It is a philosophy that has built one of Asia's most formidable property empires, and one that continues to guide every acquisition, every development decision, and every patient year of holding.